Saturday, March 6, 2010

True Religion is a BUY for Svigals and Tall Firs Portfolios

Hooray! I did something well I guess. People seemed very impressed with the revenue model. I have my professor and this class to thank for my new found ability to quickly and accurately predict future events, (OK, maybe not so accurately sometimes). But yeah, we'll probably make a roughly 20 to 30 thousand dollar investment based off a report I did, which I think is pretty exciting. I don't know if everything I projected going forward is going to come to fruition, but I did the best I could. My estimates weren't all that far off from the mean on Wall Street. I arrived at a target price of $30.69 and the average analyst estimate had the stock priced at $29.87, with a high of $34 and a low of $27. So anyway, I'm pretty happy with myself right now. It's a little bit of validation for this whole "education" thing that I'm paying for.

Unemployment Report

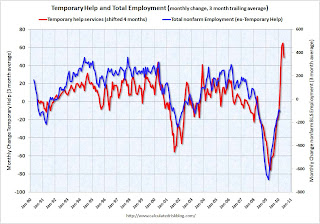

No significant change. 36,000 jobs lost, 9.7% unemployment rate holds steady. The one semi-interesting development has been the surge in hiring of temporary workers. Over 100,000 temporary jobs have been added in the last two months alone. Below is a graph via Calculated Risk charting temp hiring (4 months shifted) against actual hiring without temps.

It shows about a four month lag between temp hiring and actual employment growth. Judging from the activity we've seen in temporary labor, we would expect to see some positive jobs news in the near future. The logic behind this is simple, following a recession firms will increases hours of current employees and hire temporary workers before making any permanent changes. It's still difficult to tell what's going to happen, but I would say that seeing growth in temporary labor is definitely better than not seeing growth. The economy is still in a depressed state. 9.7% unemployment is way too high. State governments will not be able to maintain public services if they're losing that kind of revenue and the federal government will not be able to maintain unemployment benefits to that number of people without further increases in the deficit.

It shows about a four month lag between temp hiring and actual employment growth. Judging from the activity we've seen in temporary labor, we would expect to see some positive jobs news in the near future. The logic behind this is simple, following a recession firms will increases hours of current employees and hire temporary workers before making any permanent changes. It's still difficult to tell what's going to happen, but I would say that seeing growth in temporary labor is definitely better than not seeing growth. The economy is still in a depressed state. 9.7% unemployment is way too high. State governments will not be able to maintain public services if they're losing that kind of revenue and the federal government will not be able to maintain unemployment benefits to that number of people without further increases in the deficit.

In general, this report didn't give me a lot of reason to be optimistic. All the pundits seem to be declaring we've "reached bottom," which is great and all, but they were saying the same thing 6 months ago. The most significant part of the stimulus package is behind us, fed emergency programs are unwinding, and the economy is going to have to stand on its own two feet. It just seems like broadly, there are a lot more headwinds out there than tailwinds, that is, more factors are putting downward pressure on the economy than upward pressure.

It shows about a four month lag between temp hiring and actual employment growth. Judging from the activity we've seen in temporary labor, we would expect to see some positive jobs news in the near future. The logic behind this is simple, following a recession firms will increases hours of current employees and hire temporary workers before making any permanent changes. It's still difficult to tell what's going to happen, but I would say that seeing growth in temporary labor is definitely better than not seeing growth. The economy is still in a depressed state. 9.7% unemployment is way too high. State governments will not be able to maintain public services if they're losing that kind of revenue and the federal government will not be able to maintain unemployment benefits to that number of people without further increases in the deficit.

It shows about a four month lag between temp hiring and actual employment growth. Judging from the activity we've seen in temporary labor, we would expect to see some positive jobs news in the near future. The logic behind this is simple, following a recession firms will increases hours of current employees and hire temporary workers before making any permanent changes. It's still difficult to tell what's going to happen, but I would say that seeing growth in temporary labor is definitely better than not seeing growth. The economy is still in a depressed state. 9.7% unemployment is way too high. State governments will not be able to maintain public services if they're losing that kind of revenue and the federal government will not be able to maintain unemployment benefits to that number of people without further increases in the deficit.In general, this report didn't give me a lot of reason to be optimistic. All the pundits seem to be declaring we've "reached bottom," which is great and all, but they were saying the same thing 6 months ago. The most significant part of the stimulus package is behind us, fed emergency programs are unwinding, and the economy is going to have to stand on its own two feet. It just seems like broadly, there are a lot more headwinds out there than tailwinds, that is, more factors are putting downward pressure on the economy than upward pressure.

Friday, March 5, 2010

Fed Watch: Deflation

Question...

I don't understand what's going on here. How exactly do we go about reconciling large increases in PPI and import prices with the .1% decrease in core CPI? Are consumers simply unable to hold the burden of increased input prices? And if this is the case, why on earth are producers, specifically in the manufacturing sector, making large investments in new capital and spending on labor? (OK yes its temp labor for the most part but still.) Basically, why the ramp up in production without significant signs of returning demand? I'm not following.

I get the "inventory bounce" argument. I see the connection between "slack" in the broader economy leading to deflationary pressures. So what's with the input price increases? That's the part I don't understand. The only way prices on the producer side can be increasing, is if there is demand for such inputs. If there's demand for the inputs, producers must see consumer side demand out there somewhere. I guess I'm just not seeing it. I agree that the fed should probably be more concerned about deflation, especially considering the events we've seen in Japan, coupled with the fact that deflation can lead to the whole "debt-deflation" death spiral situation. But despite this, manufacturers are going all Jean Baptiste Say on me. I thought we were past this theory in like 1860, why is it still around? It's the old saying "if you build it, they will come," I'm just not sure from where they'll be coming considering the economic environment for the average consumer.

I don't understand what's going on here. How exactly do we go about reconciling large increases in PPI and import prices with the .1% decrease in core CPI? Are consumers simply unable to hold the burden of increased input prices? And if this is the case, why on earth are producers, specifically in the manufacturing sector, making large investments in new capital and spending on labor? (OK yes its temp labor for the most part but still.) Basically, why the ramp up in production without significant signs of returning demand? I'm not following.

I get the "inventory bounce" argument. I see the connection between "slack" in the broader economy leading to deflationary pressures. So what's with the input price increases? That's the part I don't understand. The only way prices on the producer side can be increasing, is if there is demand for such inputs. If there's demand for the inputs, producers must see consumer side demand out there somewhere. I guess I'm just not seeing it. I agree that the fed should probably be more concerned about deflation, especially considering the events we've seen in Japan, coupled with the fact that deflation can lead to the whole "debt-deflation" death spiral situation. But despite this, manufacturers are going all Jean Baptiste Say on me. I thought we were past this theory in like 1860, why is it still around? It's the old saying "if you build it, they will come," I'm just not sure from where they'll be coming considering the economic environment for the average consumer.

Thursday, March 4, 2010

True Religion Apparel, Inc.

My UOIG project was on a premium retail company... Still not sure how I feel about that considering the broader economic environment. Of course, by that I mean, falling home prices/sales with high unemployment contributing to an increased savings rate as families try to repair household balance sheets and rebuild equity in their homes subsequently causing a squeeze on disposable income which directly affects premium apparel retailers like True Religion... That was quite a sentence.

I built a revenue model for the company using a lot of the techniques we've learned in class. It was cool to take my basic knowledge of econometrics/forecasting and combine it with my basic knowledge of equity valuation.

I haven't blogged much this week, and that report is a pretty big reason as to why. If you missed it the first time, here's another link to the same thing.

I built a revenue model for the company using a lot of the techniques we've learned in class. It was cool to take my basic knowledge of econometrics/forecasting and combine it with my basic knowledge of equity valuation.

I haven't blogged much this week, and that report is a pretty big reason as to why. If you missed it the first time, here's another link to the same thing.

Subscribe to:

Comments (Atom)